The main contract between the Client and Contractor for general building/construction type projects is the Engineering and Construction Contract. It is subdivided into options, of which the Client will choose either option A, B, C, D, E or F. This bulletin will consider the specific elements of option C & D for both tendering purposes and administering a live project.

An overview to options C & D – These options are “Target Cost” type contracts, option C based on an Activity Schedule and option D based on a Bill of Quantities. It is chosen by Clients who generally have a less well-developed Scope, and therefore it is not sensible to let under fixed price type contracts (options A or B) where the Contractor would have to price significant risk.

Option C Activity Schedule: The Contractor is expected to produce the Activity Schedule. In simple terms this is a case of breaking the project down into several items, allocating costs against each of those items, with the sum of the items adding up to represent the overall tender price (the Prices). The Activity Schedule will then be referenced in contract data part 2 as to where it is included within the tender submission, which in turn forms part of the signed contract. The “Price for Work Done to Date” (the application) that the Contractor can claim for each period is NOT based on completed items on the Activity Schedule like it is for option A. The Contractor is paid each period the Defined Cost (referred to as the “Price for Work Done to Date”), based upon the applicable elements within the Schedule of Cost Components, less any disallowed costs. This will be the actual cost that they can prove that they have incurred up until the date of the application plus the Fee, and also include a forecast of the Defined Cost up until the next application date. The Fee is calculated by multiplying the fee percentage in contract data to the amount of Defined Cost. There will also be a deduction for any Disallowed Costs, which are explained in more detail below. There is no mechanism (or need) to revise the Activity Schedule under option C during the life of the project as its only purpose is to ascertain the original target price.

Option D Bill of Quantities: The Client is expected to produce the Bill of Quantities and it should be included within the documents given to a Contractor at tender stage. This is different to option C, where it is the Contractor who will produce the equivalent Activity Schedule used in that type of contract.

In simple terms the Bill of Quantities is produced by breaking the project down into a number of items, and then stating the expected quantity of each item that is anticipated to be required. Contract data part 1 will identify the method of measurement (the measurement techniques followed) that has been used to create the Bill of Quantities. The Contractor will then be able to state a unit rate based on that quantity, and by multiplying the quantity by the rate will give a projected cost of that line item. The sum of all the line items added together represents the overall tender price (the Prices). The Bill of Quantities can also include single lump sum items where the rate will be a single amount. The Contractor will state within contract data part 2 where within their submission the completed Bill of Quantities is, which will form an integral part of the signed contract.

The Contractor is paid each period Defined Cost based upon the Schedule of Cost Components less any Disallowed Costs (referred to as the “Price for Work Done to Date”). This will be the actual cost that they can prove that they have incurred up until the date of the application plus Fee, and also include a forecast of the Defined Cost up until the next application date. The Fee is calculated by multiplying the fee percentage in contract data to the amount of Defined Cost. There will also be a deduction for any Disallowed Costs, which are explained in more detail below. There is no mechanism (or need) to revise the Bill of Quantities under option D during the life of the project as its only purpose is to ascertain the original target price.

Option C and D assessing the target share percentage: The Contractor prepares forecasts of the total Defined Cost for the whole of the works at the intervals stated in Contract Data. For a majority of projects this forecast would be at each application, but for larger projects could be every three months. This means that there will be a regular assessment during the life of the project as to the actual amount spent and the forecasted remaining cost left to go and hence if predicting to be under or over the target price.

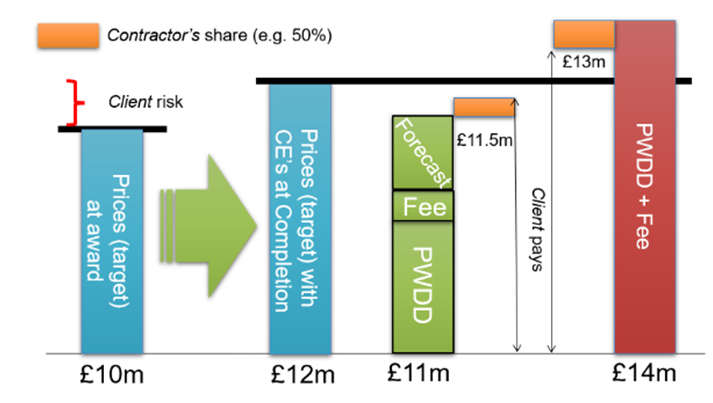

Option C and D share percentage: The Contractor share percentage is only assessed at the end of the project. An initial calculation is carried out and paid in the application following the achievement of Completion, and a final calculation/adjustment done at the last application when all the final costs have been assessed at the defect date. The share percentage will be stated in contract data part 1 and could be a simple 50%/50% or 60%/40% split, or could be broken down into bandings with a different Contractor share percentage for each banding: For example, the final Price for Work Done to Date coming in at 90-110% of the target may be 50% Contractor share, but then 25% Contractor share for anything under 90% and 75% Contractor share for anything over 110%. This means the Contractor gets paid less (gain) share if they are significantly under the target, but then take more (pain) share if they are significantly over the target. The target will be adjusted during the life of the project with the value of implemented compensation events, which can increase or decrease the target accordingly.

Disallowed Costs (for both options C and D)

Disallowed Costs are defined in clause 11.2(26) and as the names suggest are costs that can be disallowed from what the Contractor is claiming each period. It is important therefore for everyone in the Contractor’s team to understand what these are so that they can avoid them being incurred and affecting the amount that they will be paid overall. Some of the more significant ones are costs that:

- are not justified by Contractor records and accounts

- was incurred because the Contractor did not give an early warning

- correcting defects after Completion

- Plant and Materials not used to Provide the Works

- Resources not used to Provide the Works

Although classed as disallowed cost they will technically still be shared costs, as whilst not being paid as part of Defined Cost, will increase the share percentage that the Contractor will be paid (depending on the Contractor share percentage at that point). Therefore, the Client is still sharing to some degree, the risk of disallowed costs with the Contractor. This is also an area where through Z clauses the Client may add extra elements that would also be Disallowed costs, so important to check and understand these amendments for any specific project.

Compensation Events: Unless by agreement, Activity Schedule rates (option C) or Bill of Quantity rates (option D) will not be used to assess compensation events. They will be built up from first principles using the Schedule of Cost Components. An Activity Schedule or Bill of Quantities does not need to be revised every time a compensation event is agreed. It will just be added to the “bottom line” of the Activity Schedule/Bill of Quantities. The Prices at any one point in time will be the original total at tender stage, plus the value of any implemented (agreed) compensation events. It should be essential to both Parties to want to agree compensation events in a timely manner so that the target (the Prices) can be adjusted to give a reasonable understanding if the Contractor is above or below the target at any point in time. If it is taking a long time to agree compensation events the forecast cost may well exceed the target and appear that the Contractor is overspending.

Schedule of Cost Components: This is used under options C and D to not only assess compensation events but also the applications each period, and therefore a bit more detailed than the Short Schedule of Cost Components used for options A and B. It is made up of eight categories that the Contractor would be able to claim relevant costs for when assessing their Defined Cost each period (typically every four weeks or monthly):

- People – more detailed than the Short Schedule of Cost Components and built up from first principles rather than pre-agreed People Rates that are used in options A and B. The NEC4 2023 amendments also include more specific rules to allow for people working from home which is now much more common post-Covid

- Equipment – e.g. amounts for hire of equipment, charge out rates for Contractor owned equipment, price for consumed equipment, price for transporting to/from the working area.

- Plant and Materials – for all permanent works that are installed such as pipework, cladding, cabling etc

- Subcontractors – a new category for NEC4 where Subcontractors costs can now be included as a lump sum, rather than having to break it down into the other categories listed

- Charges – for example, services into the site to run offices welfare, disposal of materials from site, charges for access to the Working Areas

- Manufacture and Fabrication – rates for people involved in manufacture and fabrication of Plant and Materials outside the Working Areas

- Design – rates for people involved in design done outside the Working Areas, as well as cost of travel expenses when entering the Working Areas

- Insurance – which only confirms that you cannot claim for insurable events or insurance premiums

Value Engineering: NEC4 has added in a new process entitled “Contractor’s proposals”. Where a scheme is a Client design, a Contractor can offer a quotation for a saving where they are able to recommend a value engineering proposal and share in the resultant saving. There is no “value engineering percentage” for options C and D (like there is for options A and B) but any such saving will just be calculated as part of the pain/gain share calculation at the end of the project.

Differences with the Engineering and Construction Subcontract (ECS) The Contractor should be looking to pass their contractual obligations with their supply chain on a back-to-back basis. The ECS allows the Contractor to do exactly that. The rules, principles and even clause numbers are almost identical in the ECS as they are in the ECC. Everything in this bulletin therefore applies to the Subcontractor in relation to their Contractor if they are engaged under an ECS option C or D. The only real changes between the ECC and ECS are that the names of the Parties change (from Client/Contractor to Contractor/Subcontractor), and that some of the timescales change for a Subcontractor to do something within, and for the Contractor to respond. A Contractor engaged with their Client under option C or D does not have to choose the same option for their Subcontractor. They may consider that by the time they are procuring that Subcontractor, that the risk profile is better understood and more manageable by the Subcontractor so can choose option A or B for that contractual arrangement.

Summary: Option C and D contracts are a shared risk contract between the Client and Contractor. The Contractor is paid on an actual cost basis plus their fee and at the end of the project any underspend or overspend is shared between the Parties in accordance with the agreed percentages in Contract Data. These contracts are more administrative compared to options A and B as they are an open-book type contract, and all costs must be proved/verified along the way. Disallowed costs need to be understood and avoided so that a Contractor maximises their financial entitlement on the project. The regular agreement of compensation events should be important to both Parties so they both know where they stand in terms of forecast cost compared to the target.